How to Purchase Reverse Mortgage and Improve Your Quality of Life

How to Purchase Reverse Mortgage and Improve Your Quality of Life

Blog Article

Unlock Financial Liberty: Your Guide to Acquiring a Reverse Home Loan

Recognizing the intricacies of reverse mortgages is vital for house owners aged 62 and older seeking financial flexibility. As you consider this option, it is vital to realize not only how it works however also the ramifications it may have on your monetary future.

What Is a Reverse Home Loan?

The basic charm of a reverse mortgage exists in its prospective to enhance economic adaptability during retirement. Property owners can use the funds for numerous functions, consisting of medical expenses, home renovations, or daily living costs, therefore offering a security net throughout a crucial stage of life.

It is crucial to understand that while a reverse home loan enables for boosted cash circulation, it additionally lowers the equity in the home over time. As rate of interest accumulates on the exceptional financing equilibrium, it is essential for possible borrowers to thoroughly consider their long-lasting monetary strategies. Consulting with a financial consultant or a reverse mortgage specialist can offer valuable understandings into whether this option lines up with an individual's financial goals and situations.

Eligibility Requirements

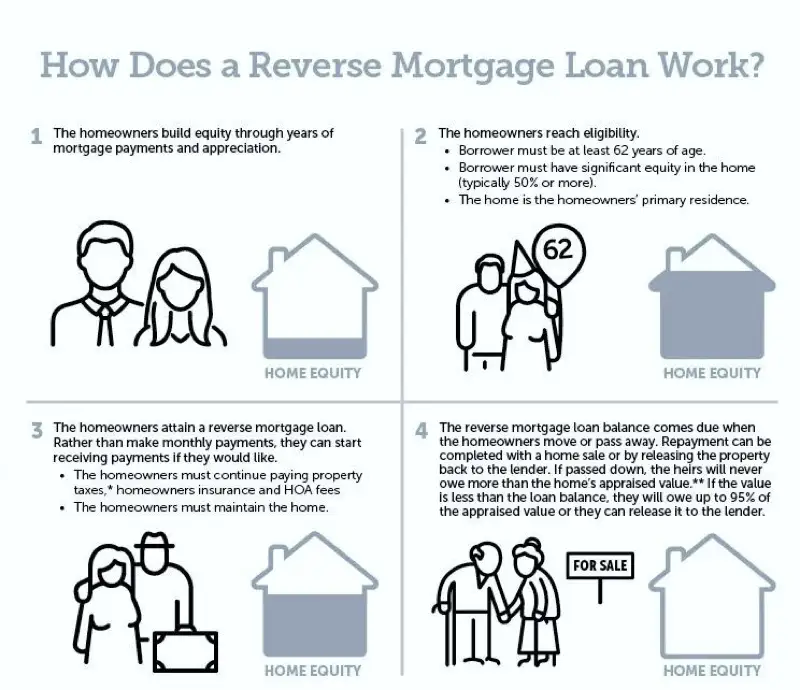

Comprehending the qualification needs for a reverse home mortgage is crucial for home owners considering this monetary choice. To certify, candidates must go to the very least 62 years of ages, as this age criterion permits elders to gain access to home equity without month-to-month home mortgage payments. In addition, the house owner must inhabit the house as their primary residence, which can consist of single-family homes, certain condos, and produced homes meeting specific standards.

Equity in the home is another important demand; house owners normally need to have a significant amount of equity, which can be figured out via an appraisal. The amount of equity offered will directly affect the reverse home loan quantity. Candidates must show the ability to maintain the home, including covering building tax obligations, property owners insurance coverage, and maintenance costs, making sure the residential property continues to be in good problem.

In addition, possible borrowers should undergo an economic evaluation to evaluate their revenue, debt history, and overall economic circumstance. This analysis aids lenders identify the applicant's capacity to fulfill continuous responsibilities connected to the residential property. Fulfilling these needs is essential for securing a reverse home mortgage and making sure a smooth economic change.

Advantages of Reverse Mortgages

Countless advantages make reverse home mortgages an attractive choice for elders looking to enhance their monetary versatility. purchase reverse mortgage. Among the primary advantages is the capability to transform home equity right into cash money without the demand for month-to-month home mortgage settlements. This attribute allows elders to accessibility funds for different demands, such as clinical costs, home improvements, or daily living prices, consequently alleviating monetary anxiety

In addition, reverse mortgages supply a safety net; seniors can remain to live in their homes for as long as they satisfy the loan needs, cultivating stability during retired life. The profits from a reverse home mortgage can additionally be made use of to delay Social Security benefits, potentially leading to higher payments later.

In addition, reverse home mortgages are non-recourse fundings, implying that borrowers will certainly never owe even more than the home's worth at the time of sale, shielding them and their successors from economic obligation. The funds visit this web-site received from a reverse home loan are generally tax-free, including another layer of monetary relief. Generally, these advantages position reverse mortgages as a sensible option for elders seeking to boost their monetary situation while preserving their treasured home setting.

Fees and costs Included

When considering a reverse mortgage, it's necessary to be conscious of the different prices and charges that can impact the overall financial image. Comprehending these costs is critical for making a notified decision about whether this monetary product is best for you.

Among the primary expenses connected with a reverse home loan is the source fee, which can differ by lender however typically ranges from 0.5% to 2% of the home's appraised value. Additionally, homeowners should prepare for closing costs, which might consist of title insurance Read Full Article policy, assessment fees, and credit rating report costs, normally amounting to several thousand bucks.

An additional substantial expenditure is home loan insurance premiums (MIP), which protect the lending institution versus losses. This cost is usually 2% of the home's worth at closing, with a continuous annual premium of 0.5% of the staying financing balance.

Finally, it is necessary to take into consideration ongoing costs, such as real estate tax, house owner's insurance policy, and upkeep, as the consumer continues to be in charge of these expenditures. By carefully evaluating these costs and costs, homeowners can much better assess the financial ramifications of pursuing a reverse mortgage.

Actions to Get Started

Starting with a reverse home mortgage entails a number of key steps that can aid improve the procedure and ensure you make educated decisions. Evaluate your monetary scenario and identify if a reverse home mortgage straightens with your lasting objectives. This consists of reviewing your home equity, existing financial debts, and the necessity for additional earnings.

Following, research different lenders and their offerings. Seek respectable organizations with favorable reviews, transparent charge frameworks, page and competitive rate of interest. It's important to contrast problems and terms to find the best fit for your requirements.

After selecting a loan provider, you'll require to finish a detailed application process, which generally requires paperwork of revenue, assets, and residential or commercial property details. Participate in a therapy session with a HUD-approved counselor, that will supply understandings right into the ramifications and obligations of a reverse home mortgage.

Final Thought

In verdict, reverse home loans offer a viable choice for senior citizens seeking to boost their financial security during retired life. By transforming home equity right into accessible funds, house owners aged 62 and older can address numerous financial requirements without the pressure of month-to-month payments.

Understanding the ins and outs of reverse home mortgages is important for house owners aged 62 and older seeking economic liberty.A reverse home mortgage is a financial item developed largely for property owners aged 62 and older, allowing them to convert a portion of their home equity right into cash - purchase reverse mortgage. Consulting with a reverse mortgage or a monetary consultant expert can give important insights right into whether this choice lines up with a person's financial goals and circumstances

Moreover, reverse mortgages are non-recourse fundings, suggesting that debtors will certainly never owe more than the home's value at the time of sale, protecting them and their successors from economic obligation. Overall, these benefits setting reverse mortgages as a useful option for senior citizens looking for to improve their monetary scenario while preserving their treasured home environment.

Report this page